Unit4 Financials by Coda 2026Q2

Unit4 Financials by Coda 2026Q2R2 was made available on 15th June 2026.

The following enhancements and fixes are included in this maintenance release:

Electronic Invoicing – Life Cycle Tracking (Inbound CDAR API)

A new REST resource has been introduced for Electronic Invoicing life cycle tracking. This resource captures and records status updates received in CDAR format from the certified service provider (PA/PDP).

For further details, please refer to the Electronic Invoicing Life Cycle API documentation.

Fixes

- Bug 1101870 – Resolved an issue where the workflow typescope was missing in the 2026Q2 release. The typescope is now included, enabling workflow definitions to be successfully imported during installation and upgrades.

Highlights of the 2026Q2 release include:

Administration:

Trusted Certificates Master

A new Ignore invalid certificates setting has been introduced, allowing IPPS protocols to ignore any certificate warnings or errors on the endpoint when it is enabled. The default is enabled.

Output Protocols

The IPPS protocol can use the Trusted Certificates Master to verify the remote server certificate. When ‘Ignore invalid certificates’ is enabled, warnings and errors about the certificate are ignored for this protocol.

Certificate Master

A new certificate master has been added to store third party certificates. Each certificate master stores a single encrypted certificate.

OpenID Connect User Claims

The user can now upload claims via a CSV file, allowing claims to be updated in bulk.

My Profile and User Master Changes

Language Labels and Fields

The existing Default language label has been renamed to Translated names language to better reflect its purpose. This setting determines which language is used for translated element names when configured on the element master.

A new Display language field has been introduced, allowing users to control the language of the user interface independently of browser settings.

System Security – Password Parameters

The user can now specify a message transport master and sender e-mail address on System Security – Password Parameters.

This will enable the system to notify a user when their password has been changed ensuring compliance with C5 audit requirements.

Finance:

Document Master

A new check box has been added to the document master to enable life cycle tracking for use with inbound and outbound electronic invoicing.

Electronic Invoicing:

Mapping Master

The Invoice Matching Mapping Master now supports mapping multiple values for Order numbers, Advice note numbers, Comments and Printable comments when an XPath returns multiple results.

Identifying the Supplier Using PartyIdentification

The AccountingSupplierParty/Party/PartyIdentification/ID element in the UBL is now supported as a supplier identifier for posting invoices and credit notes.

Electronic Invoicing Life Cycle API

A Document Life Cycle API is now available, for use with inbound and outbound electronic invoicing. The API can ADD and LIST Life Cycle events for Finance and Billing documents.

Posting Invoices as Credit Notes

UBL InvoiceTypeCode 384 is now configured by default to be posted as a Credit Note in Finance and Invoice Matching.

Miscellaneous:

Query Performance

Query performance on Microsoft SQL Server has been improved by removing CAST expressions when selecting ID columns.

Technical:

Deprecated features:

IBM Platforms

IBM platforms are deprecated as of this release. See release notes for more details.

Implicit Flow

The ‘Implicit’ flow authentication method has been deprecated and will be removed in a future release. The final release has not been determined. We recommend that the ‘Authorization Code with PKCE’ flow is used instead when configuring a system to use OpenID Connect authentication.

.NET router

The .NET router has been deprecated. The final release has not been determined.

The Integration Toolkit Command Centre module

The Integration Toolkit Command Centre module (ITK) has been deprecated and will be removed in a future release. The final release has not been determined.

JavaScript User Extension Implementation Support

The ability to implement User Extensions using JavaScript is deprecated. The final release to include this support has not been determined.

Note: Support for implementing User Extensions using Java is not deprecated and is the recommended approach for implementing User Extensions.

Coda Encrypter

The command line utility coda-encrypter.exe is deprecated. The final release to include this support has not been determined.

Removed features:

32-bit XL was removed in the 2025Q1 release. Please use the 64-bit XL. This means that the supported releases of XL are available as 64-bit only.

Support for Apple Safari has ended. It is recommended to use Google Chrome or Microsoft Edge.

Security Updates

- The security of Print Formatter and Workflow Designer has been improved in this release. It is recommended that users install the versions available for download from the web application.

- A new configuration setting, com.coda.common.app.security.initialPassword.maxDays, has been introduced to control the expiry of first‑use passwords that are set or reset by an administrator.

- The third-party libraries Microsoft Azure Client Library for Identity and Key Vault Secrets have been updated to address a security issue (CVE-2025-67735).

- The version of the Unit4 Message Hub Bridge has been updated to fix vulnerabilities CVE-2026-1225 & CVE-2026-33870.

- The third-party libraries jackson-core, jackson-annotations, jackson-databind have been updated to improve security. This addresses WS-2026-0003.

- The third-party library BouncyCastle has been updated to improve security. This addresses CVE-2026-0636.

General Fixes/Updates:

- The Table Link Transfer Client now honours standard JVM proxy configuration such as ‑Dhttps.proxyHost.

- Exporting the Capability Settings report to Excel when using a non-English language no longer fails with an error about invalid sheet names.

- An Asset can now be created in a category that has comments of more than 100 characters long mapped from a Finance document.

- Assets PostRuleMaster Web Service can now be used in Workflow definitions.

- The deletion of attachments is now correctly audited, when using Audit Trail.

- Browse Details no longer fails when an External Reference URL contains a $ character.

- A comment field configured as mandatory on an Invoice Matching input template master is now correctly enforced during Input.

- Structured output processing has been enhanced to support increased data volumes for the GDPdU transformation type.

- Incorrect total values are no longer generated when using the UBL 2.1 Invoice and Credit Note Transformations.

- An issue has been resolved where the get-period-from-date REST API endpoint rejected date values containing a time zone offset in the form +hh:mm.

- Changes have been made to some REST API endpoints such that they display the same error text as those from the SOAP API rather than just the error code.

- The Currency Calculation XMLi service is now correctly visible in the Functional Security capability tree for read-only capability profiles.

Further details on the new features, security updates and reported issues can be found in the release documentation.

The release documentation for this release (and previous releases) can be found in the documentation area on the community.

The software can be downloaded from the “Software” tab on Community4U.

Are you making the most of Unit4 Financials by Coda?

Our Systems Health Check is designed to help you identify areas where you may be able to improve performance and ensure you extract the maximum benefit from your investment in Unit4 Financials by Coda.

Strengthening Auditability and Control Over Retail Revenue Through Automated Reconciliation

Strengthening Auditability and Control Over Retail Revenue Through Automated Reconciliation

Trintech Case Study

Close the Sales Audit Gap From Store to Bank to Your ERP

Trintech automates over 90% of daily matching cross-channel transactions for the world’s largest retailers.

The Retail Challenge

Modern retailers live in a world of multiple POS systems, payment processors, wallets, and banks. With intensified scrutiny on transaction accuracy and data protection, every day you’re trying to mitigate crucial issues:

- Did everything we sold in person and online actually make it to the bank?

- Do cash and card activity match what’s in the GL/ERP and other systems?

- Where are we leaking margin through shrink, fees, timing issues, and write-offs?

When the answers depend on spreadsheets and monthend fire drills, variances are harder to trace, exceptions age, and losses pile up. Your sales audit becomes reactive – finding leaks after the money’s gone, rather than proactively preventing them.

Unit4 Financials by Coda 2026Q1

Unit4 Financials by Coda 2026Q1 was made available on 10th March 2026.

Highlights of the 2026Q1 release include:

Administration:

Trusted Certificates Master

A new Trusted Certificates Master has been added to store and manage public trusted certificate files. These certificates can subsequently be used by various protocols such as HTTPS, IPPS, or SFTP to establish trust for external servers. The Trusted Certificate Master will be used by the protocols described in a later release.

Unique index column updated to not-nullable – com_extconfig

The column itemname in the com_extconfig table has been updated to not-nullable to allow primary keys to be added for database table replication purposes.

Generic Browse Master

The user can now specify a Printing Options Master on the General tab of the Generic Browse Master.

Finance:

Reminder Letters

The Print or Transmit process for reminder letters can now access the Printing Options Master on the Generic Browse master.

This will allow the reminder letter filename to be set to the value specified on the Printing Options Master.

Pay/Collect Master

The Printing process now displays the default Printing Options Master which is held on Printing tab of the Pay/Collect Master for Remittance output.

Structured Output:

UBL 2.1 Invoice Transformation and UBL 2.1 Credit Note Transformation

The ability to add multiple notes for the EN16931 schema for France (BG-1) vocabulary has been added to the Invoice and Credit Note Transformations. The vocabulary is available on the EN16931 Schema and is configured on the Manipulation Master.

Electronic Invoicing:

Posting to Companies with Balancing Elements

You can now post invoices and credit notes to a company using balancing elements, while using the VAT number to identify the company and balancing element level 1.

Identifying the Company Using EndpointID

The AccountingCustomerParty/Party/EndpointID element in the UBL is now supported as a company identifier for posting invoices and credit notes.

Console:

Authentication

A new read-only field Financials web application URL has been added to the Authentication configuration. The value of this field is configured in the Configuration tab and is displayed here for reference only.

Miscellaneous:

Attachment Deletion

Improvements have been made to how attachments are deleted. The system start up runs a background process that periodically polls to identify and remove any attachments that need deleting.

Software Media Changes

Changes have been made to how software media is delivered for on-premise customers. Instead of a single ISO containing the software and documentation this has been split to make downloads more efficient and gives you flexibility to access only the content you need.

Technical:

Deprecated features:

Implicit Flow

The ‘Implicit’ flow authentication method has been deprecated and will be removed in a future release. The final release has not been determined. We recommend that the ‘Authorization Code with PKCE’ flow is used instead when configuring a system to use OpenID Connect authentication.

.NET router

The .NET router has been deprecated. The final release has not been determined.

The Integration Toolkit Command Centre module

The Integration Toolkit Command Centre module (ITK) has been deprecated and will be removed in a future release. The final release has not been determined.

JavaScript User Extension Implementation Support

The ability to implement User Extensions using JavaScript is deprecated. The final release to include this support has not been determined.

Note: Support for implementing User Extensions using Java is not deprecated and is the recommended approach for implementing User Extensions.

Coda Encrypter

The command line utility coda-encrypter.exe is deprecated. The final release to include this support has not been determined.

Removed features:

32-bit XL was removed in the 2025Q1 release. Please use the 64-bit XL. This means that the supported releases of XL are available as 64-bit only.

Support for Apple Safari has ended. It is recommended to use Google Chrome or Microsoft Edge.

Security Updates

- The Password hashing algorithm has been updated to comply with Cloud Computing Compliance Criteria Catalog (C5) requirements

- The version of the Unit4 Message Hub Bridge has been updated to fix vulnerabilities.

- User-supplied PDF attachments are rejected if JavaScript actions are found in the PDF.

- The XMLi Java Router no longer accepts XML that makes use of external entities.

General Fixes/Updates:

- An issue copying and pasting items within Print Formatter has now been resolved.

- Background Financials tasks now use a keep alive setting to prevent failure of long running tasks.

- The Capability Master selection of available Message Transport Masters on the Alerts tab has been optimised, improving performance and preventing failures.

- The credit lines on the Financials document are now referenced on the Asset transaction when depreciating, instead of the debit lines. This was a problem when depreciating multiple periods and having “Post all asset transactions to this period” set.

- A timestamp error no longer occurs when sending recurring documents with attachments to Workflow.

- A special character ‘?’ can now be entered when adding a document comment using Diary and Browse Transactions.

- The pay write process now correctly handles EncodeForXMLOutput, which no longer applies to a literal value from a conditional element.

- Invoices with attachments that go into matching and have a discrepancy raised against them, which is greater than the document threshold, are now successfully sent to workflow for authorisation.

- Electronic Invoicing now supports Finance Document masters which use Automatic-by-period numbering.

- The parsing of XML inputs has been improved. Greater attention is now paid to namespace declarations. This resolves intermittent issues including errors creating requisitions and errors invoking the Tax service public API.

- When using OpenID Connect authentication, SOAP API calls will use the default user if that user is also mapped to special users (INSTALL, LEVEL8, LEVEL8SUB). This change also applies when using the Mobile Apps for workflow authorisations.

- REST API calls can now be executed by users with passwords containing non-ASCII characters.

- SOAP API calls can now be executed by users with passwords containing non-ASCII characters.

- REST API calls can now retrieve masters with codes that contain special characters such as { } and ( ).

- When using the Element Master XMLi API, the Get, Update and Set operations will now return all the mandatory fields in the response if an error occurs.

Further details on the new features, security updates and reported issues can be found in the release documentation.

The release documentation for this release (and previous releases) can be found in the documentation area on the community.

The software can be downloaded from the “Software” tab on Community4U.

Are you making the most of Unit4 Financials by Coda?

Our Systems Health Check is designed to help you identify areas where you may be able to improve performance and ensure you extract the maximum benefit from your investment in Unit4 Financials by Coda.

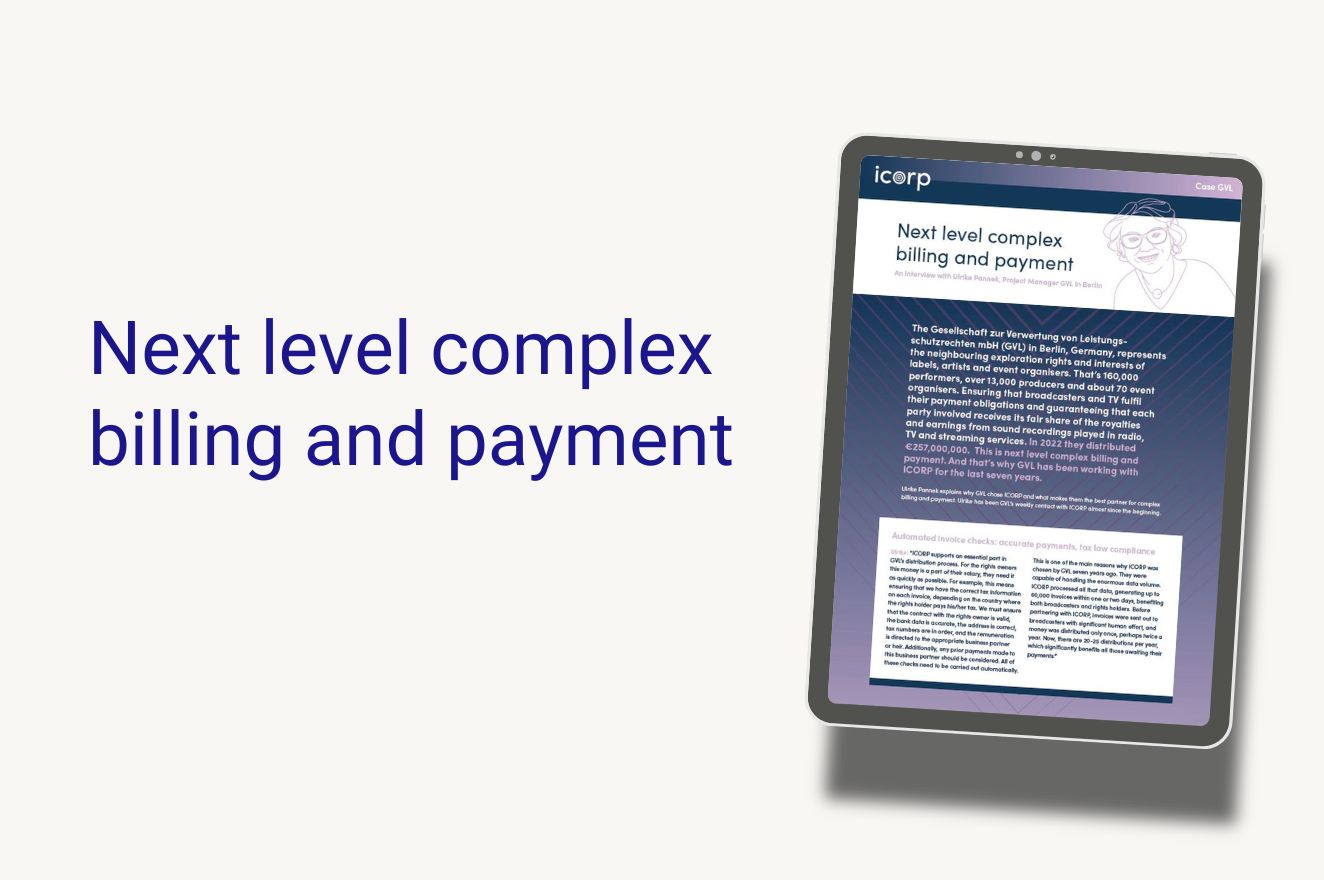

Next level complex billing and payment

Case Study

Next level complex billing and payment

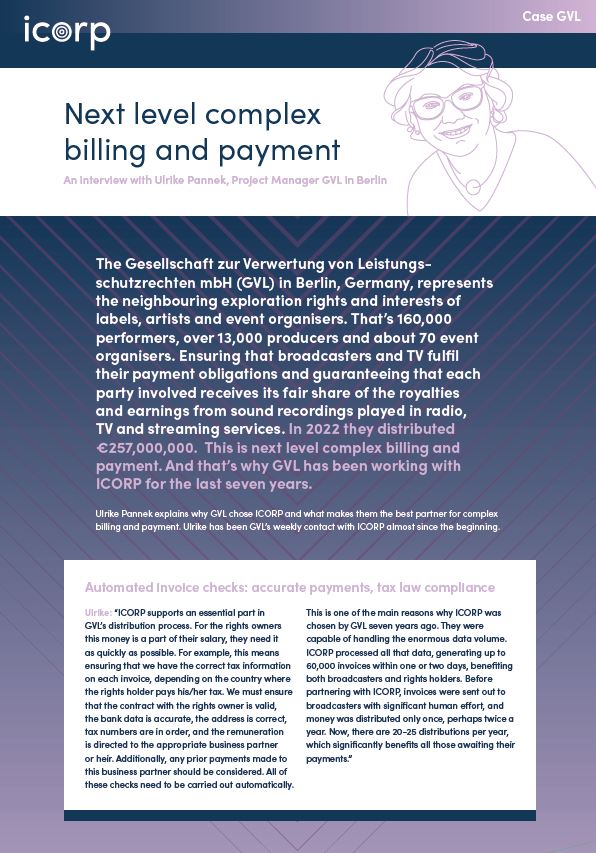

The Gesellschaft zur Verwertung von Leistungsschutzrechten mbH (GVL) in Berlin, Germany, represents the neighbouring exploration rights and interests of labels, artists and event organisers. That’s 160,000 performers, over 13,000 producers and about 70 event organisers. Ensuring that broadcasters and TV fulfil their payment obligations and guaranteeing that each party involved receives its fair share of the royalties and earnings from sound recordings played in radio, TV and streaming services. In 2022 they distributed €257,000,000. This is next level complex billing and payment. And that’s why GVL has been working with ICORP for the last seven years.

Ulrike Pannek explains why GVL chose ICORP and what makes them the best partner for complex billing and payment. Ulrike has been GVL’s weekly contact with ICORP almost since the beginning.

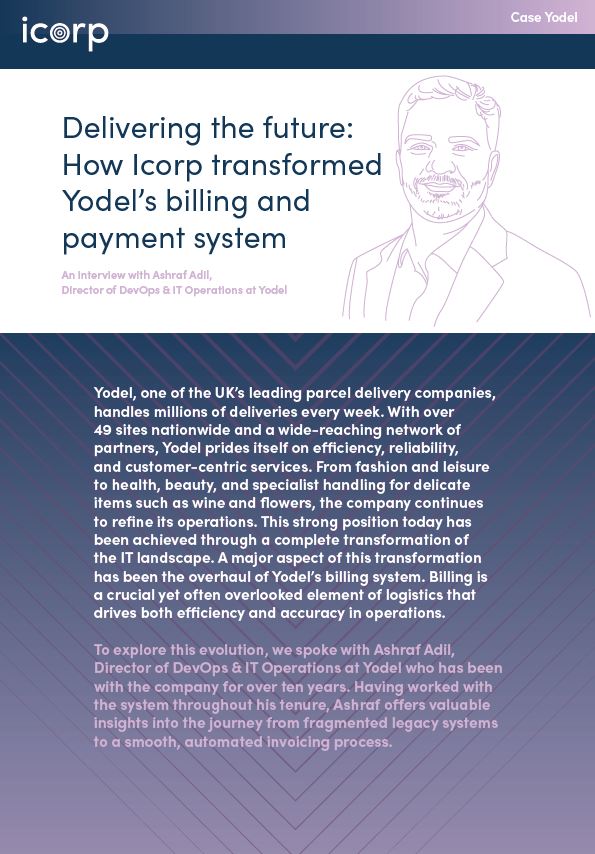

Delivering the future: How Icorp transformed Yodel’s billing and payment system

Case Study

Delivering the future: How Icorp transformed Yodel’s billing and payment system

Yodel, one of the UK’s leading parcel delivery companies, handles millions of deliveries every week. With over 49 sites nationwide and a wide-reaching network of partners, Yodel prides itself on efficiency, reliability, and customer-centric services. From fashion and leisure to health, beauty, and specialist handling for delicate items such as wine and flowers, the company continues to refine its operations. This strong position today has been achieved through a complete transformation of the IT landscape. A major aspect of this transformation has been the overhaul of Yodel’s billing system. Billing is a crucial yet often overlooked element of logistics that drives both efficiency and accuracy in operations.

To explore this evolution, we spoke with Ashraf Adil, Director of DevOps & IT Operations at Yodel who has been with the company for over ten years. Having worked with the system throughout his tenure, Ashraf offers valuable insights into the journey from fragmented legacy systems to a smooth, automated invoicing process.

Unit4 Financials by Coda 2025Q4

Unit4 Financials by Coda 2025Q4 was made available on 2 December 2025.

Highlights of the 2025Q4 release include:

Finance:

Pay/Collect Master

The user can now specify a Printing Options Master on the Printing tab of the Pay/Collect Master for Remittance output.

The Remittance filename will be set to the value specified on the Printing Options Master. If no Printing Options Master is specified, or the master has no filename, the existing naming functionality is applied.

Interest Charges

You now have the ability to define a minimum charge value on the Interest Master.

The minimum charge on the Interest Master is applied when an interest proposal is generated. If a minimum charge is present, then no summary will be generated if the home currency charge is less than the minimum charge value.

Element Master

On the Electronic Invoicing tab, the balancing element level account mappings are now hidden. When the Company balancing element level is set to 1, Element 1 in the account mapping is not accessible. When the Company balancing element level is set to 2, Element 1 and Element 2 in the account mapping are not accessible.

Pay

For Pay Write when sending a Pay file via HTTP POST, the file name generated will be sent as the ‘X-U4F-Filename’ header.

Structured Output:

Run Process

A Structured Output process can now be run via the public API.

Technical:

Deprecated features:

Implicit Flow

The ‘Implicit’ flow authentication method has been deprecated and will be removed in a future release. The final release has not been determined. We recommend that the ‘Authorization Code with PKCE’ flow is used instead when configuring a system to use OpenID Connect authentication.

.NET router

The .NET router has been deprecated. The final release has not been determined.

The Integration Toolkit Command Centre module

The Integration Toolkit Command Centre module (ITK) has been deprecated and will be removed in a future release. The final release has not been determined.

JavaScript User Extension Implementation Support

The ability to implement User Extensions using JavaScript is deprecated. The final release to include this support has not been determined.

Note: Support for implementing User Extensions using Java is not deprecated and is the recommended approach for implementing User Extensions.

Coda Encrypter

The command line utility coda-encrypter.exe is deprecated. The final release to include this support has not been determined.

Removed features:

32-bit XL was removed in the 2025Q1 release. Please use the 64-bit XL. This means that the supported releases of XL are available as 64-bit only.

Support for Apple Safari has ended. It is recommended to use Google Chrome or Microsoft Edge.

Security Updates

- Encryption improvements have been applied to the Punchout password when using the Element Master API.

- The third-party libraries commons-compress and commons-lang3 have been updated to improve security. This addresses CVE-2025-48924.

- The third-party libraries nimbus-jose-jwt have been updated to improve security. This addresses CVE-2025-53864.

- A potential security issue in a service used by Customiser has been fixed.

- CSV export has been improved to prevent Formula Injection. Fields exported in a CSV which start with ‘=’ (which identifies a formula) are now pre-fixed with a single quote.

- Downloading desktop clients via a direct access URL is now only available when the necessary functional security permissions are enabled.

General Fixes/Updates:

- The data dictionary now lists all possible log types for table com_loghead.

- The Unit4 Table Link Transfer Client now processes the oas_linkelement and oas_linkhead tables last and marks the records as transferred after all records have been successfully transferred for a table.

- The Unit4 Table Link Transfer Client parameter ‘Batchsize’ now has a default value of 10000.

- Interaction with the OpenID Connect identity provider has been improved.

- An issue in the write stage of a payment run that resulted in the bank rejecting the file has now been resolved. This was related to XML output encoding and Unicode conversion handling a special character for example &.

- Reminder letters sent via FTP/SFTP now appends a date and timestamp to the file name to make it unique.

- An issue where changes to matched invoices in Invoice Maintenance failed to post to Finance when involving deferred or partially recoverable tax has been resolved. The system now correctly processes and posts these updates.

- Structured Output no longer creates zero size, zero content files when outputting to the repository or SFTP.

- The following changes have been made to the IV3 transformation in Structured Output :-

- The ‘Metadata Periode’ now allows 0 and 5 to selected as stated by the CBS matrix

- The data view column is no longer mandatory

- The missing ‘Ultimo’ figures have been added to the JSON output file

- The Generic Browse API is no longer restricted by the browse limit configured in the application (capability/console). An optional parameter, rowLimit, is now available to limit the rows returned by the API. If this is not specified or is set to 0 then no limit is applied.

- The ‘/finance/currency/currency/get-rates/{cmpCode}/{rateDate}’ Rest API Endpoint no longer returns an index out of bounds error.

- The ‘/finance/pay/pay/get-dtt/{cmpCode}/{userCode}/{proposalCode}/{payMasterCode}’ Rest API Endpoint no longer returns an index out of bounds error.

- The ‘/finance/browsedetails/browsedetails/get-line/{cmpCode}/{code}/{number}/{lineNumber}’ Rest API Endpoint no longer returns an index out of bounds error.

Further details on the new features, security updates and reported issues can be found in the release documentation.

The release documentation for this release (and previous releases) can be found in the documentation area on the community.

The software can be downloaded from the “Software” tab on Community4U.

Are you making the most of Unit4 Financials by Coda?

Our Systems Health Check is designed to help you identify areas where you may be able to improve performance and ensure you extract the maximum benefit from your investment in Unit4 Financials by Coda.

SMTP Modern Authentication Migration

SMTP Modern Authentication Migration

Update

As part of the ongoing security enhancements, Basic Authentication for SMTP Client Submission in Exchange Online (Office 365) will be permanently disabled by Microsoft. Microsoft has postponed the enforcement date, and the new deadline is now end of December, 2026. However, we strongly encourage you to complete this transition as soon as possible.

If your organization currently uses Basic Authentication to send emails via Office 365, you must transition to a modern authentication method or an alternative solution before this date to avoid disruption.

Please note that this is a mandatory change from Microsoft and cannot be postponed or overridden by Unit4. Systems or applications that continue to use Microsoft Office 365 Basic Authentication will no longer be able to send emails after this date.

For official Microsoft information, visit: Updated Exchange Online SMTP AUTH Basic Authentication Deprecation Timeline | Microsoft Community H…

For any questions or guidance regarding this change, please contact Unit4 Customer Support, referencing this notice in the subject line.

Published March 2026

As part of the ongoing security enhancements, Basic Authentication for SMTP Client Submission in Exchange Online (Office 365) will be permanently disabled by Microsoft, effective March 1, 2026.

If your organization currently uses Basic Authentication to send emails via Office 365, you must transition to a modern authentication method or an alternative solution before March 1, 2026, to avoid disruption.

Please note that this is a mandatory change from Microsoft and cannot be postponed or overridden by Unit4. Systems or applications that continue to use Microsoft Office 365 Basic Authentication will no longer be able to send emails after this date.

For official Microsoft information, visit: Exchange Online to retire Basic auth for Client Submission (SMTP AUTH) | Microsoft Community Hub

For any questions or guidance regarding this change, please contact Unit4 Customer Support, referencing this notice in the subject line.

Published December 2025

Why choose Millennium for Unit4 Financials by Coda?

We are an Elite Unit4 Partner with more than three decades of experience working with Unit4 Financials by Coda. That means we have the knowledge and experience to design, implement and support the right Unit4 Financials solution for your business.

Unit4 Release Schedules 2026

Unit4 Release Schedules 2026

Unit4 Financial Planning & Analysis Release Schedule 2026

Please find below the preliminary release schedule of FP&A 2026

| 2026 | Non-production (Preview & Acceptance) | Production |

| Q1 | 17th of March | 25th/26th of April |

| Q2 | 16th of June | 25th/26th of July |

| Q3 | 15th of September | 24th/26th of October |

| Q4 | 8th of December | 23rd/24th of January (2027) |

- Data Center: SaaS Azure

- Product: U4FPA

- Deployment option: Shared, Dedicated

- Environment types: Production, Preview, Acceptance

Please note that this is a preliminary schedule and is subject to change.

ERP CR Release Schedule 2026

Please find below the preliminary release schedule of ERP CR 2026

| 2026 | Preview | Acceptance | Production |

| Q1 | 16th of March | 27th of April | 23rd/24th of May |

| Q3 | 14th of September | 26th of October | 21st/22nd of November |

- Regions: Worldwide

- Products: ERP CR

- Data Center: SaaS Azure

- Deployment option: Shared, Dedicated

- Environment types: Preview, Acceptance, Production

| 2026 | Non-production (Preview & Acceptance) | Production |

| Q1 | 16th of March | 25th of May |

| Q3 | 14th of September | 23rd of November |

- Regions: Nordics

- Products: ERP CR

- Data Center: Nordics

- Deployment option: Public, Dedicated

- Environment types: Preview, Acceptance, Production

Please note that this is a preliminary schedule and is subject to change.

Detailed overview of release scope and hourly schedule will be published after the official Release announcement on Community4U.

Unit4 Financials by Coda Continuous Release

Please find below the preliminary release schedule of Unit4 Financials by Coda 2026

| 2026 | Preview | Acceptance | Production |

| Q1 | 17th of March | 24th of March | 25th/26th of April |

| Q2 | 16th of June | 23rd of June | 25th/26th of July |

| Q3 | 15th of September | 22nd of September | 24th/25th of October |

| Q4 | 8th of December | 15th of December | 23rd/24th of January (2027) |

- Data Center: SaaS Azure

- Product: U4F

- Deployment option: Shared, Dedicated

- Environment types: Preview, Acceptance, Production

Please note that this is a preliminary schedule and is subject to change.

Unit4 ERPx Release Schedule 2026

Please find below the preliminary release schedule of ERPx 2026

| 2026 | Non-production (Preview & Acceptance) | Production |

| Q1 | 16th of March from 05:00 am to 05:00 pm UTC – United States/Australia/Norway

17th of March from 05:00 am to 05:00 pm UTC – Europe/United Kingdom/Canada |

18th of April from 05:00 pm to 19th of April 05:00 am UTC – All regions |

| Q2 | 15th of June from 05:00 am to 05:00 pm UTC – United States/Australia/Norway

16th of June from 05:00 am to 05:00 pm UTC – Europe/United Kingdom/Canada

|

18th of July from 05:00 pm to 19th of July 05:00 am UTC – All regions |

| Q3 | 14th of September from 05:00 am to 05:00 pm UTC – United States/Australia/Norway

15th of September from 05:00 am to 05:00 pm UTC – Europe/United Kingdom/Canada

|

17th of October from 05:00 pm to 18th of October 05:00 am UTC – All regions |

| Q4 | 7th of December from 05:00 am to 05:00 pm UTC – United States/Australia/Norway

8th of December from 05:00 am to 05:00 pm UTC – Europe/United Kingdom/Canada |

16th of January 2026 from 05:00 pm to 17th of January 2026 05:00 am UTC – All regions |

Please note that this is a preliminary schedule and is subject to change.

Why choose Millennium for Unit4?

As an Elite Unit4 Partner with over three decades of experience in Change Management, we bring expertise in designing, implementing, and supporting the right Unit4 solution for your business. Unlock the full potential of your Unit4 solution by partnering with Millennium – your trusted transformation partner.

Getting the Most from Coda: The Unit4 Financials Task App

Published November 2025

At Millennium, we asked our teams across the globe to look back at our last 100 projects. We asked them to think about the lessons that have stood out, the topics that crop up most often, the problems they’ve encountered, the things that have gone well (and the things that haven’t!).

The result? A fascinating collection of insights into technology, process, and, most importantly, people. Because here’s the truth: people are at the heart of every great business. The best tech doesn’t replace them – it empowers them.

Over the next few blog posts, we’ll be sharing the top four themes that emerged, covering:

Apps, AI, People and Security

App: In the first of a series of guides based on the real-life experiences of the Millennium team, we take a closer look at the often-overlooked Unit4 Financials Tasks App.

AI: Helping you look beyond the hype, to consider how AI can make a difference to your business and how it might shape Coda in the future.

People: We look at one of the most common people-related pitfalls our teams face and how you can avoid it.

Security: Time and again, we see that, no matter how strong your firewalls and other defences are, people are the weakest link in any business’s cybersecurity. We consider some of the most valuable steps you can enact right now to protect not just Coda, but your broader data estate.

Business Apps and The Big Picture

We recently did a Microsoft Teams call. At the customer’s end, it began with about half a dozen project team members in the same meeting room. By the end of it, between the school run and getting out of the city, one by one, each of the participants had left the room. But the meeting continued all thanks to the ability to switch seamlessly to a mobile app. That’s the thing about mobile applications: at their best, they enable “business as usual”, but with an added helping of employee-focused flexibility.

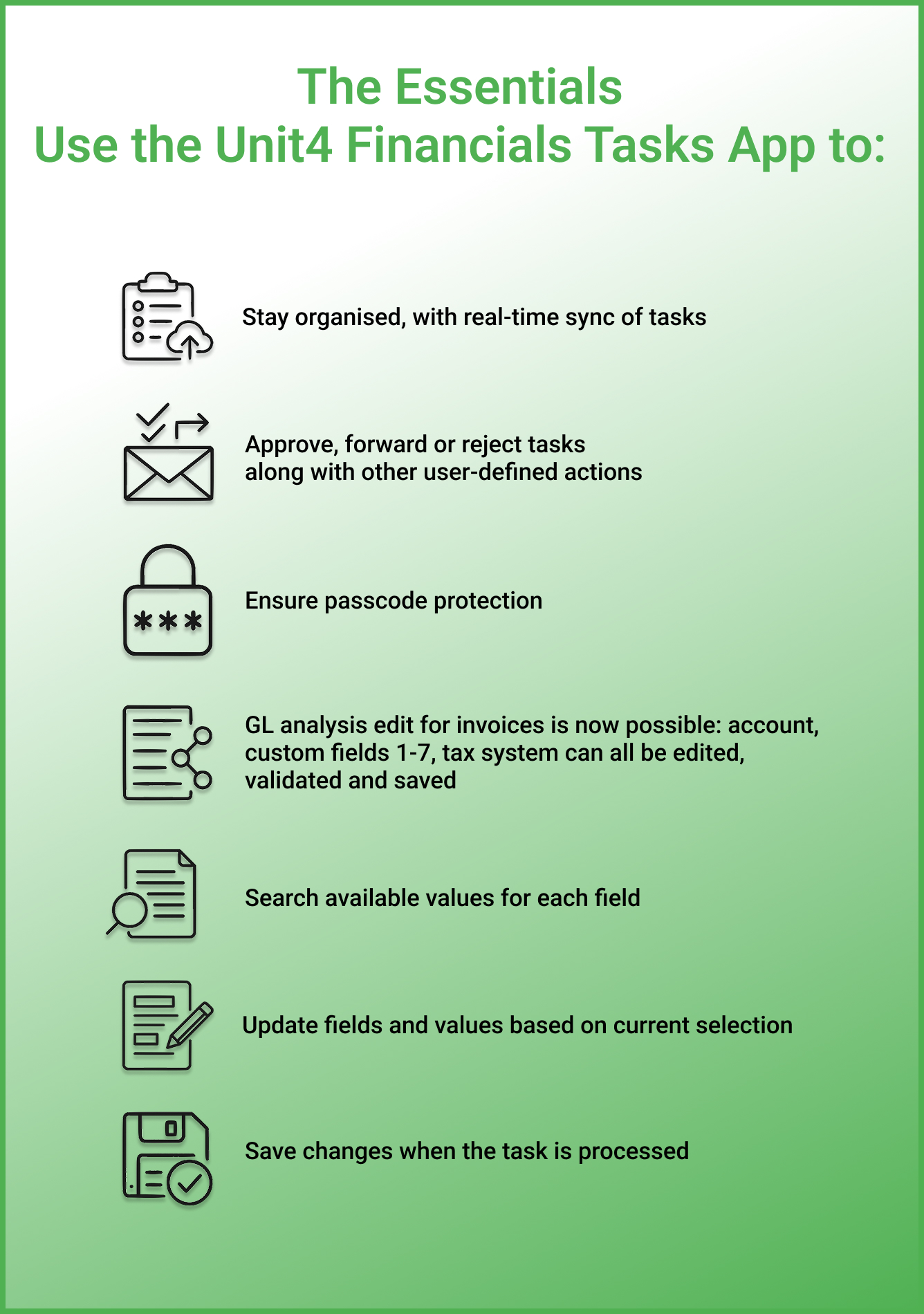

The Unit4 Financials Task App

The Unit4 Financials Tasks App enables you to view, manage, and respond to your financial tasks in real-time and from anywhere.

It eliminates friction. Connecting directly to Coda in real time, users can stay on top of their tasks wherever they are.

You can get everything you need done (and approved). Whether it’s a purchase order, a supplier change, a fresh transaction or all manner of other time-sensitive financial tasks, the app allows you to view, manage, respond and approve from anywhere.

You are always up to date. Because it allows you to access Coda directly, you can edit a range of information (e.g. general ledger information relating to transactions), including real-time updates and values synced with the Unit4 system.

What Next?

Download the Unit4 Financials Task app from the Apple or Android store.

Ready to get more out of Coda through implementation or wider rollout of the Tasks app? To get up and running rapidly, speak to us today.

3 ways to drive operational performance in renewable energy

Infographic

3 ways to drive operational performance in renewable energy

Explore this IFS infographic for three proven ways to improve operational performance in renewable energy and address common challenges.