Benefits of the automation of manual processes in Unit4 Financials

23 ways to automate and reduce cost and risk, by setting up the automation of manual processes in Unit4 Financials

January 2022

Workflow

With more people working remotely, re-configuring workflow allows organisations to keep efficient by ensuring each process is streamlined and everyone interacts with the process at the right time.

Banking payment XML

Reduce manual effort by setting up XML bank payment files.

Intercompany PO’s

Setting up intercompany PO’s will stop the need for companies to raise separate PO’s one-by-one in each company. With the Intercompany facility it is possible (for example) to raise a PO in one company that is for goods services in two other different companies.

Unit4 XL reporting

Set up reports in Unit4 XL for real-time reporting from Unit4 Financials and reduce any unnecessary manual Excel work.

Auto VAT Calculation

VAT can be calculated automatically based upon the VAT code being supplied – therefore reducing the input burden being placed on the user.

Derived fields

The entry of documents can be assisted greatly using derived fields on the input templates. This can automate the population of many of the fields on the Input screens which will speed up data entry and enhance the user experience.

Allocation

Allocation provides a flexible, automatic means of allocating centrally incurred costs across an organisation's operating units, so reducing manual work.

Currency Revaluation

The automation of currency revaluation enables you to recalculate home (GBP) values based on foreign values. The foreign values are selected, either from details or from balances, for reconversion at new exchange rates.

Account Summaries

Account summary is a user configured enquiry form that allows information from suppliers to be brought together with transaction details, balance, and diary information to produce a single view of the data.

Electronic remittances

In Continuous Release, electronic remittances can be generated automatically by email during a payment run.

Element Authorisation

Element authorisation can be used to automate new vendor and/or customer authorisations and creation.

Automatic accruals

There is an automatic routine within the invoice matching module that can create accruals and post to the financials module, so reducing month end effort.

Archiving

Archive enables the user to remove old data from the books to an internal archive area within the database. The archive process improves the system performance experienced by a user by reducing the amount of information held on the books.

Attachments

The attachments framework allows a user to attach documentary evidence to element masters, financial documents, purchase orders and sales invoices. The information can be in a variety of formats eg spreadsheet, PDF, Word etc that provides working papers or backup to a transaction. Once attached, the user can also view, remove, or replace the attached file.

Service Desk

Reduce cost and risk with Unit4 Financials Support and Maintenance from the Millennium Service Desk team.

Interface Manager

Interface Manager gives control back to the finance team to run and schedule their own interfaces so alleviating members of the IT department of doing these tasks.

Unit4 Travel & Expenses

Streamline and automate the expenses process, giving you more control over costs, better enforcement of company policy and help reduce the time and effort it takes to process employee or subcontractor expenses.

AutoCash

Save time and effort by automating your bank statement processing – automatically load, post, match and reconcile any items on your Bank Statements with transactions recorded in Unit4 Financials.

Unit4 Purchasing & Invoice Matching

Enforcing the authorisation and control over expenditure at the start of the process, rather than after the fact on receipt of invoice helps companies to stick to their budgets, control costs and gain efficiencies from better supplier leverage.

Unit4 Invoice Capture

Unit4’s Invoice Capture automates the capture and posting of invoices through intelligent OCR scanning and posts directly into Unit4 Financials.

Data Cleansing

Data cleansing removes major errors and inconsistencies that are inevitable when multiple sources of data are pulled into one dataset. Using tools to clean-up data makes the process more efficient since you will be able to quickly get accurate information into your system of choice.

Asset uploading

Do you regularly need to upload assets into Unit4 Financials fixed assets module – if so then Millennium’s Asset Uploader can streamline this process to help ensure all your assets are loaded error free.

Data Migration

Migrate your data between systems or to the Cloud, giving you quicker integration, faster implementation, and reduced risk.

Contact us for further details

Looking for ways to automate and reduce cost and risk? Submit your details and one of our experts will be in touch.

Archiving for Unit4 Financials

Archiving for Unit4 Financials

With any accounting or financial management solution, regular archiving helps you keep control over the size of your datasets, speed up processing times and ensure ongoing optimum software performance.

In this blog post, discover how archiving works in Unit4 Financials by Coda and the difference between the two types of archiving available.

What are the Archiving options in Unit4 Financials?

There are two types of archiving:

Internal archiving

With internal archiving, information continues to reside within your main Unit4 Financials production database.

Tables in the internal archive are given an “arc” prefix. The transactions within these internally-archived tables can still be accessed through enquiries. To search archived items, all you need to do is change your selector to ‘archive’ instead of ‘books’.

External archiving

External archiving involves moving data from the Unit4 Financials production database to a separate archive database. Note however, that this archive database still resides on the same database server. As with internal archiving, externally archived data is held in “arc” tables. To do external archiving, you first must do internal archiving.

How to utilise Archiving for Unit4 Financials

With any accounting system, the larger the dataset, the longer it takes to process requests (e.g. queries, searches and transactional reports). Especially if your Unit4 Financials users are experiencing a gradual drop-off in response speed over time, it’s a sign that archiving is likely overdue.

To avoid having to routinely process potentially millions of lines of irrelevant data for each request, it’s certainly worth focusing on the following:

• Establishing an archiving policy

Matters to consider here include whether and how often users need to query data that is over a year or two old. You should also look at how often your AP/AR teams need to query transactions paid/matched over a year ago.

• Ensuring a correct archiving set-up

As a start, you need to ensure the archiving feature in your Unit4 Financials system has been activated and configured according to your needs.

Does archived data remain accessible?

In short, yes. When you have archived your data in Unit4 Financials, that data remains searchable.

When you submit a query on the system, you have the option to search live data only, or include archived data. For most users, the majority of day-to-day queries relate only to recent data. So for these queries, users can stick with the default live data search setting. Regular archiving means that the system does not have to trawl through swathes of irrelevant data, thereby helping to maintain optimal search response times on routine tasks. On those occasions where you need to check historical data, you can simply switch the query type to include archived information.

Unit4 Financials Archiving: Watch how it works…

This brief video further illustrates the differences between each archiving method to help you choose between the two. It covers the issues that commonly arise in archiving financial information and how you can resolve them within the system. We also share a case study illustrating the benefits of archiving.

(Published January 2022)

As an Elite Unit4 Partner, Millennium Consulting provides expert input to ensure Unit4 Financials is fully aligned to your organisational requirements. For help with archiving a backlog of legacy data, devising an archive policy, or optimising your existing archive processes, speak to us today.

Business Change in 2022

Business Change in 2022

January 2022

The financial crisis of 2008 fundamentally altered the environment for the Financial Services industry and since then banks and insurance companies have spent hundreds of £ millions on regulatory compliance initiatives.

In the insurance world for example, IFRS 17 will continue at the forefront of insurance companies thinking until 2023 and beyond. Designed to achieve the goal of consistent, principle-based accounting for insurance contracts, IRFS17 requires insurers to integrate data from across their organisation and create a single version of the truth. However, the “golden source” data created not only enables them to meet their regulatory obligations but also to access granular data that was previously inaccessible. It is a classic case of the law of unintended consequences.

In December 2021, the International Accounting Standards Board (IASB) issued Initial Application of IFRS 17 and IFRS 9—Comparative Information (Amendment to IFRS 17). The amendment is a transition option relating to comparative information about financial assets presented on initial application of IFRS 17. The amendment is aimed at helping insurers to avoid temporary accounting mismatches between financial assets and insurance contract liabilities and therefore improve the usefulness of comparative information for financial statement users. (https://www.ifrs.org/projects/completed-projects/2021/initial-application-ifrs-17-and-ifrs-9-comparative-information-amendments-to-ifrs-17/)

2022 is likely to be a challenging year for the insurance industry. For jurisdictions working towards a 2023 effective compliance date, the pressure has increased and the next six months will be critical if the deadline is to be met.

Millennium Consulting believes that compliance with the new regulation can allow insurers to become disrupters, digitise their processes and fundamentally re-engineer their Target Operating Models.

So, whether your actions are driven by regulatory compliance or from the desire to adopt best practice, Millennium is here to help. Our team are experienced financial markets professionals with deep domain expertise, be it products, market mechanisms or the business and regulatory drivers that are shaping the industry. Working with many of the world’s leading financial markets and insurance companies we help them define, manage and deliver the change they need to achieve market leadership.

What’s new in Unit4 Financials Continuous Release?

December 2021

What’s new in Unit4 Financials Continuous Release?

New functions rolled out under recent Unit4 Financials quarterly releases have significantly enhanced the user experience, further enabling your finance team to streamline business processes, reduce operational risk and free up resources for value-added work.

Here’s a summary of what has been added since October 2020, along with a closer look at some of the most noteworthy enhancements…

At a glance: release date summary

| CR 2021 Q4 (7th December 2021) |

| CR 2021 Q3 (14th September 2021) |

| CR 2021 Q2 (9th June 2021) |

| CR 2021 Q1 (9th March 2021) |

| CR 2020 Q4 (8th December 2020) |

| CR 2020 Q3 (14th October 2020) |

| V14 R16 (27th July 2021) |

| V14 R17 (end November 2021) |

- Hotfix to protect Unit4 Financials in the Log4j Java library

- Table Link Transfer Client

- Billing: Use Structured Output on Final Issue

- Billing: Copy Attachments on Posting

- Invoice matching: Set number of background matching threads

- Structured Output – UBL 2.1 Transformation: XML can be validated against the UBL 2.1 Invoice schema

- Attachments can now be managed from within the Billing Browse screen

- It is now possible to attach the PDF Invoice or Credit Note to the Billing document on final issue

- Scheduling a task of type Print Invoices now permits you to generate structured output for invoices (for example, XML in UBL 2.1 Transformation)

- Purchase orders approval can now be viewed across company in read-only mode

When you save masters, trailing spaces are now automatically removed. Print invoicing functionality is also improved, including support for XML formatting, as well as for invoices in pdf format.

- Documents outputs can now be written to an SFTP location

- Leading and trailing spaces are automatically removed when updating master names and short names

- The ‘Print Invoices’ function now allows an XML invoice. Transformation to be generated and sent. A pdf from a print format can be attached to the Finance document as its primary attachment

- The ‘Remove’ checkbox for additional lines in input is now positioned on the right-hand side by default

- Structured Output – UBL 2.1 Transformation: the generated XML file is now validated against the UBL Invoice schema

- Structured Output – UBL 2.1 Transformation: new vocabulary available including IBAN, attachment ID

This release included a number of enhancements that actually go a long way in improving the user experience. Examples include the new option to sort a paylist in descending order. There is also a new ‘element authorisation status’ for the financials selector master, which means that an element that isn’t authorised for changes can be excluded automatically without having to send a reminder or statement.

- Download XL for Unit4 Financials

- Document master setting to prevent the user who originally posted a document to the intray from posting the document to the books

- Pay/Collect summary now displays the pay proposal list by Pay Date in descending order

- Element authorisation status added to financials selector master

- New Punchout parameter added, user email

- Review Punchout items screen has new ‘select all’ and ‘deselect all’ buttons

- Punchout website now appears in a new tab in the browser

- Structured Output has a new transformation available, called ‘FEC’ Transformation (Fichier des ecritures compatables)

- Structured Output now allows zip file compression

- Structured Output can now generate .csv files without quotes

The new Tablelink for Cloud feature helps to simplify cloud migrations, removing the need to rewrite interfaces using web services and APIs. The release also included SFTP support, along with the ability to create comma-separated files that can be transported. e-Invoicing capabilities were also enhanced.

- Structured Output – CSV Transformation

- Structured Output – Output to SFTP

- Structured Output – Output to HTTP POST

- Tablelink for Cloud – Helper and API

- Improvements to upgrade Scripts

- e-Invoicing enhancements (Dutch XML invoice load)

- Unit4 Financials Idealization Process

Version 14 of Unit4 Financials saw the introduction of a new billing module. Among other enhancements, the 2020 Q3 continuous release saw an extension of these billing features.

- System users with OpenID Connect

- Billing – Quantities copied to Finance

- Billing – Print Preview

- Structured Output – Message Hub Output

- Unit4 Extension Kit – Samples

- Structured Output – GDPdU (local German product)

Having introduced a wide range of new features in the previous quarter, the 2020 Q2 release was focused mostly on routine product maintenance. However, there were a couple of new functions added. These were a scheduled task for reconciliation, along with changes to the Avalara export to accommodate HMRC’s ‘Making Tax Digital’ initiative.

- Scheduled task for Reconciliation

- Structured output changes – Avalara XMI export

This was the first release under Unit4’s new quarterly roll-out model (‘Continuous Release’). It introduced a wide range of new features.

- Schedule Task for hierarchy updates. You can now schedule new tasks for hierarchy updates and asset depreciation

- Submit orders on auto convert from requisitions

- Browse Transactions: Raise Corrective Journal

- Browse Transactions: Copy Document

- Deep link ‘balance’ drill to browse transactions

- Schedule Asset Depreciation

- Element template customisations copied via copy company. Element template customisations are now copied via the ‘copy company’ functionality

- Billing Copy Document

- Reconciliation Date & User. The introduction of this feature allows users to do retrospective reconciliation reports. In addition, the same level of functionality available in ‘browse details’ has also been extended to ‘browse transactions’

- Browse Transactions: Drill to Account Summary

- Browse Transactions: Edit Comment via related information panel

- Browse Transactions: Workflow Actions

- Provisional and Undo Year-End. Learn more about these features here

- Migrate customisations from test to live

- Allow change to balances on company master

- LRN Housekeeping without posting

- Reference Attachment Hyperlink as Direct Link

- GDPR for Element history

- Make use of address categories in Procurement Ordering

- Add Element Flexi-Fields data to Copy Company

- Change Pay Period. This is the ability to be able to change the period during a pay proposal

- Interco control to contain customer/supplier elements

Should you upgrade your Unit4 Financials software in 2022?

Support for Unit4 Financials V13 has already been withdrawn. Support for V14 will expire at the end of 2022. Failure to upgrade before then increases the likelihood of incurring extended support charges from Unit4.

Upgrading enables you to:

- Access the latest functionality

- Reduce operational risk and processing costs

- Continue to access Unit4’s “in support” software maintenance and support package

- Ensure you are up to date with Unit4’s latest software security package

As an Elite Unit4 Partner, Millennium Consulting specialises in delivering a seamless upgrade, while also ensuring your upgraded solution is fully aligned with organisational requirements.

Unit4 Financials Continuous Release: Provisional Year End and Year End Undo

November 2021

Unit4 Financials Continuous Release: Provisional Year End and Year End Undo

Here’s a closer look at the latest version’s new Provisional Year End and Year End Undo functions, and the benefits these will bring to your reporting procedures.

So, what has changed?

- A new Provisional Year End function. This performs all the processing of a full year end, but without closing the year in question, so you can continue posting to that year.

- A Year End Undo function. You can now undo a year end after it has been closed. Having effectively unlocked it, you are then free to post to the year in question.

Provisional Year End function

This new provisional mode option gives organisations more control over year-end. No longer do you have to wait for the auditors to give the green light before running a ‘once-and-for-all’ process. Instead, you can create and update a provisional version at any time within the system, and subsequently close it when you are ready.

If a requirement for further adjustment is flagged up after close, the undo function makes it easy to rectify it.

The new functionality is only available to users who have upgraded to Unit4 Financials 2020 / Continuously Release (previously known as Version 15). Under this latest software version, users have a choice of two modes for running a year end: provisional or full.

Undo Year End function

The new undo year end feature in Unit4 Financials Continuous Release is a further useful addition to the system’s functionality. It means you can now undo both provisional and full year ends.

When activated, the undo function cancels all year end journals posted to the final period for the latest year in which a year end has been run, as well as to the opening period of the following year. If a full year end is undone, then the minimum year will be reset to the previous year.

Benefits for finance teams

The new provisional mode gives finance officers a much greater degree of flexibility in the timing of their year end process.

Previously, launching the year end process always meant closing the year, which in turn generally meant the process could not be triggered unless and until the auditors had completed their final checks. Now, you have the option of running a report at any time of your choosing. As well as being a useful internal resource for finance, there may also be wider situations where the ability to rapidly generate a provisional year end will be useful, such as updating the executive team or providing information to external stakeholders.

Furthermore, year end close traditionally meant that the accounts for the year in question were locked down for further adjustments. The undo year end function provides a useful failsafe measure: if a discrepancy is discovered further down the line, you have the option of rectifying it quickly and easily.

Watch these new functions in action

A painless Unit4 Financials upgrade starts here

Are you currently running Unit4 Coda Financials V13 or earlier? With support for these legacy versions now withdrawn, this is the time to upgrade.

Millennium Consulting specialises not only in ensuring the upgrade process is a seamless one, but also in ensuring your upgraded solution is fully aligned with what your organisation wants to achieve. To explore your upgrade options, contact us today.

Is it time to upgrade?

Upgrading your finance software can provide new functionality, increased automation and more efficient processes.

Utilising the Homepage Portal in Unit4 Financials

November 2021

In this blog post discover how the Unit4 Financials Homepage Portal can transform the user experience, enabling easier navigation, faster processing, and more effective day-to-day task management.

The Homepage Portal is available on Unit4 Financials V12 onwards.

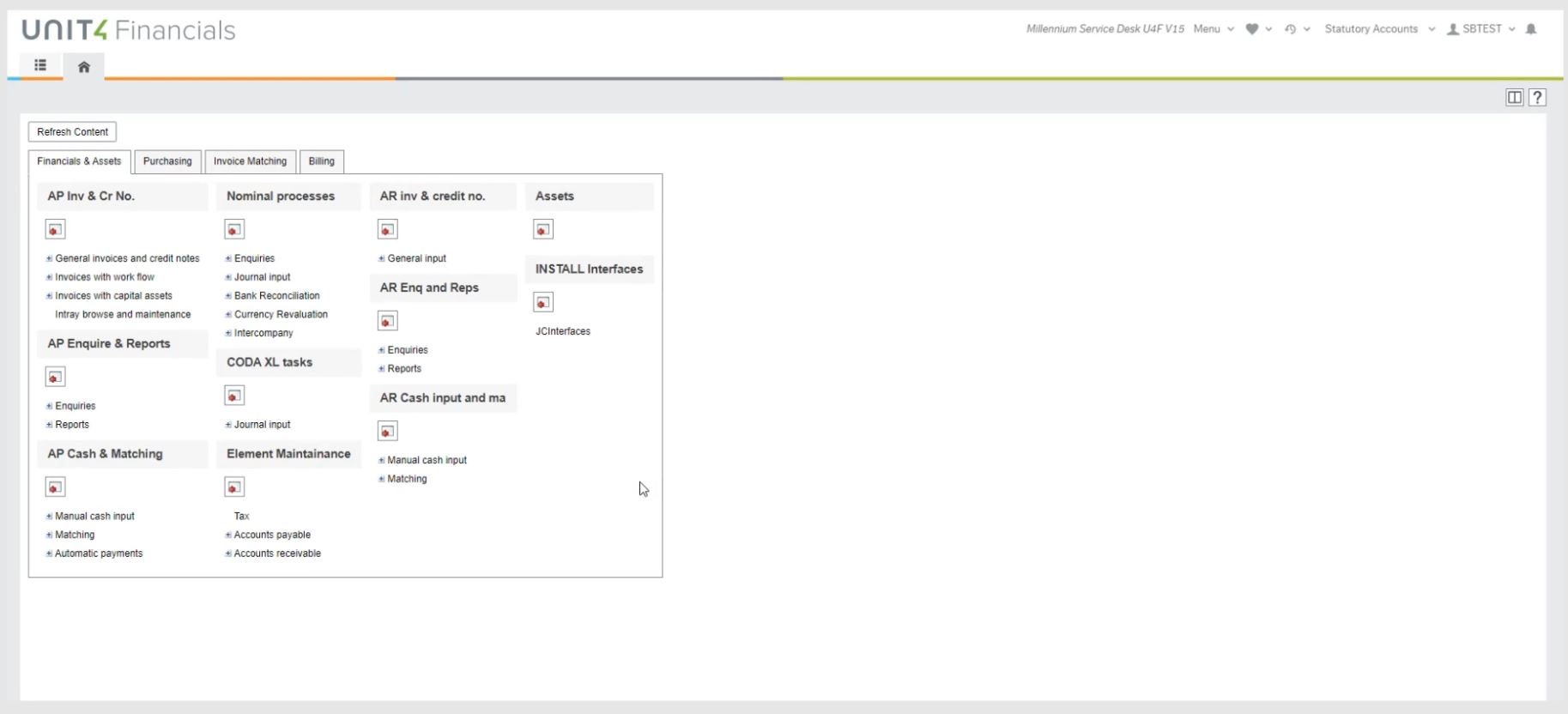

If you are a user who has been allocated a Homepage Portal, your default screen when logging onto the system will look something like this:

It’s refreshingly simple, comprising of three elements:

Tabs. The tabs are pages relating to distinct operational areas; in this case, Finance & Assets, Purchasing, Invoice Matching and Billing. The Portal is completely customisable, so you can match the tabs to the individual user’s role and responsibilities. For example, in the case of a team member whose sole responsibility is administering incoming invoices, the portal might include just a single tab: Accounts Payable.

Frames. The frames are used to group together similar content providers (see below) by subject area.

Content providers. Clicking on a content provider will take you directly to a specific report or function. For instance, under the Nominal processes frame within the Finance & Assets tab, a user can instantly navigate to Enquiries, Journal Input, Bank Reconciliation, Currency Revaluation or Intercompany Adjustments, simply by clicking on the relevant content provider.

Watch how the Portal speeds up task performance

Watch a demonstration of a search carried out from the main menu, and the same search executed via the Portal model.

The Portal approach is significantly more effective at taking users exactly directly where they need to be. There’s far less manual entry and toggling through presenters and selectors. On an individual user level, it’s quicker and easier. And once you apply it to a large finance team, all of whom execute dozens of processes and queries a day, it can make a huge difference to organisational productivity.

Portal setup

Portals are set up at system administrator-level. Before you start to set up a Portal, we recommend that you have a sketch map of the way you want the menus to be displayed, and the content.

Unlocking Unit4 Financials expertise

If you would like expert input on Homepage configuration, we’re here to help.

Whether you are looking for ‘easy wins’ from your existing setup, best practice advice on the platform’s latest functionality or a complete re-implementation, Millennium Consulting can provide the support you need. To access unrivalled expertise from a Unit4 Elite Partner, speak to us today.

Is it time to upgrade?

Upgrading your finance software can provide new functionality, increased automation and more efficient processes.

A Better Way to Work

A Better Way to Work

October 2021

In this white paper, you can learn.

- To make your people key to reconfiguring processes, regardless of IT expertise

- Real-time visibility can power better decision-making

- Automating tasks will improve efficiency

- To make your organisation more agile and adaptive

Read the white paper today to find a better way to work.

ERP Software Selection

ERP Software Selection

The promise of ERP (Enterprise Resource Planning) is a compelling one. Deploy the right solution and it can help deliver a complete view of your business, integrate processes and data, drive efficiency, boost productivity and sharpen your competitive edge.

But as with any major software implementation project, success is not guaranteed. Even a seasoned procurement manager can be captivated by the bells and whistles such as swish visualisations and impressive-sounding AI capabilities, while potentially losing sight of the nuts and bolts: i.e. the ability of the system to meet your real-life business problems.

Read our guide to identifying your best-fit solution for maximum return on investment.

We’re now registered providers with the CPD Certification Service

We’re now registered providers with the CPD Certification Service

August 5th, 2021

Millennium Consulting is pleased to announce that they are now an official registered provider with the CPD Certification Service. Established in 1996, The CPD Certification Service is the largest and leading independent CPD accreditation organisation working across all industry sectors.

This means finance professionals undertaking courses run by Millennium Consulting count towards annual professional development requirements set by professional regulators. Any delegate attending the future courses will be issued with an accredited CPD Certificate of Attendance, which they can subsequently use within their formal CPD record for a professional body, institute or employer.

Millennium is currently submitting courses for approval, and these will soon be available to book via the CPD Service.

Jeremy Lucas at Millennium Consulting said, “I am pleased to announce that Millennium Consulting is working towards being able to offer CPD certified courses to finance professionals. This is not only further confirmation of the high quality of our services but also endorses our view of the importance of good assessment practice. Our CPD programme will allows you to keep up to date with the latest industry trends and best practice, learn new skills and develop existing ones.”

Our accreditation can be verified by clicking this link: https://cpduk.co.uk/providers/millennium-consulting

How Financial Planning & Analysis Must Harness Scenario Planning to Aid Decision Making

How Financial Planning & Analysis Must Harness Scenario Planning to Aid Decision Making

July 2021

This whitepaper discusses how FP&A teams can harness the power of scenario-based planning to guide business leaders towards making informed decisions that ensure optimal performance during difficult times.

It is the responsibility of the FP&A team to guide business leaders towards making informed decisions that ensure optimal performance during difficult times. In doing so, they must harness the power of scenario-based planning. Below are the critical factors and steps in this process that we will discuss:

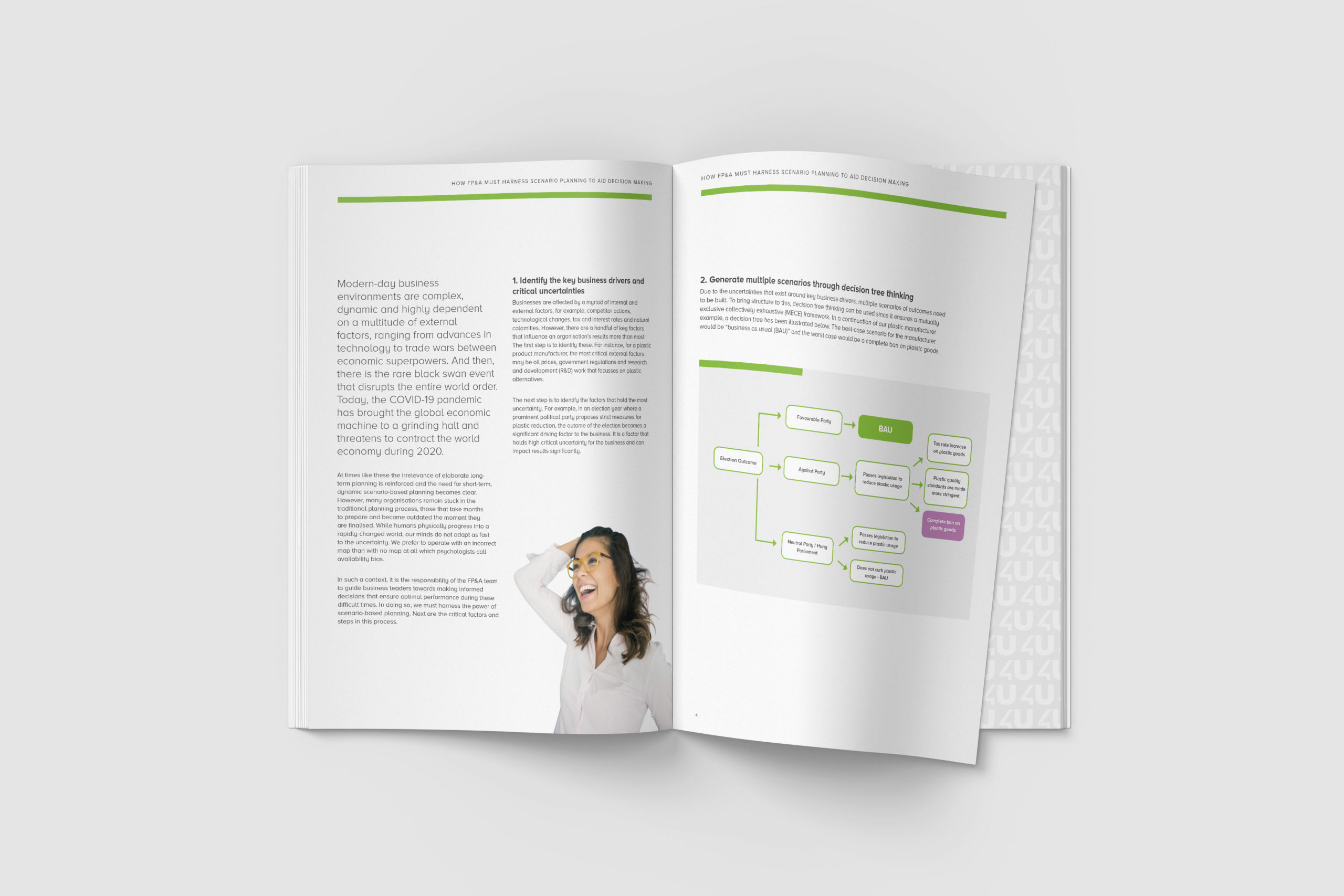

- Identifying the key business drivers and critical uncertainties.

- Generating multiple scenarios through decision tree thinking.

- Being mindful of possible cognitive errors and be receptive to the external environment.

- Harnessing the technological tools available to enable real-time planning solutions.